Sovereign Wealth Partners and InvestSense Pty Ltd

Market Commentary

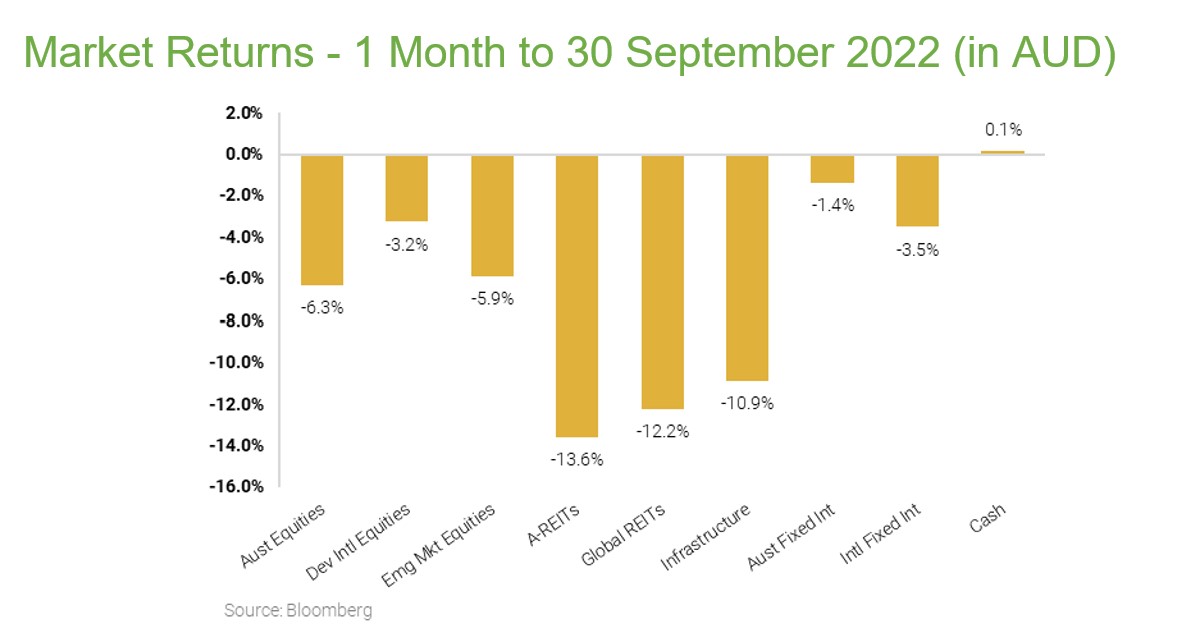

Equity markets finished the month down around 10% and around 5% for the quarter. That pretty much takes us back to the lows of mid-June for equity markets and, not coincidentally, the highs of long-term interest rates seen at the same time in June.

One thing that has changed in the last three months is that medium term inflation exceptions have actually edged down (despite the currently high inflation data), while the rate rises that are expected to be needed to make inflation fall have been revised upwards. This gets quite convoluted and more than a bit circular, but the end result is that year real (after inflation) expected rates of interest spiked in the last quarter. In essence that means that the ultra-cheap money era of the past few years could be morphing into the opposite situation where rates remain high while inflation comes down.

Credit markets and the plumbing of the financial system are particularly sensitive to real interest rates, and it was perhaps significant that signs of financial stress started to emerge in the last week of the month, particularly in the UK. There is a broad consensus that the policy announcements by the incoming Truss leadership were ill-conceived, but the Conservative Party was also arguably unlucky to be the first in the firing line as the world considered what the first thing to ‘break’ in the current hiking cycle might be. It turned out to be the Pound and the UK Gilt (government bond) market, which both fell sharply and continue to exhibit volatility to date. This then exposed frailties in the UK pension system (via funds using derivative structures to match future pension liabilities) and amongst some of the large insurance companies with exposure to illiquid credit instruments. Given that banks are better capitalised and more risk averse than they were before the GFC, investors have wondered where the risk might be hiding in this cycle and many feel that this latest episode has provided some vital clues.

In local currency terms the UK, Australian and Japanese markets have been a relative oasis of calm this year and even last quarter. However, after taking into account the strength of the US Dollar the differences are less marked and in fact with the US Dollar appreciating by 7% against the Aussie Dollar over the last three months, unhedged Australian investor’s US investments ended up level for the quarter. Southeast Asia, Europe and the US have been moving in tandem in recent months, with China leading the way down while India and Latin America have provided unusual stability and are actually up strongly for the quarter, especially on an unhedged basis (their respective currencies have also proven resilient having been forced to head off their own inflation woes in 2021).

Australian equities also had a relatively good quarter after a reasonably strong earnings season where strong dividends from the banks and miners especially trumped concerns over the economic outlook. At the other end of the ledger, real estate trusts, utilities, and other interest rate sensitive stocks like Transurban were down by about 15% a piece.

Looking Forward

This marks the third negative quarter in a row for equity markets, something which has not occurred since the GFC. For growth orientated diversified investors this is much more of a slow burn though with year-to-date losses in the low teens (diversified funds with more than 50% in equities were down by 20-40% in 2008).

For conservative investors though, this latest episode is very much on a par with the experience of the GFC as in both instances balances would have been down around 10%, but this time it has happened a bit faster and with the defensive part of the portfolio taking just as big a hit.

There is a modest silver lining though in that actively managed funds have added value and significantly cushioned the falls that we have seen relative to index funds. This was largely by choosing not to invest in government bonds and instead invest in high grade floating rate credit. There is some evidence that many stock pickers have also added value by being defensively positioned in Australia, although the evidence for overseas is less convincing with many managers having been drawn into the dominant US tech stocks that have fallen the most this year.