Sovereign Wealth Partners and InvestSense Pty Ltd

Market Commentary

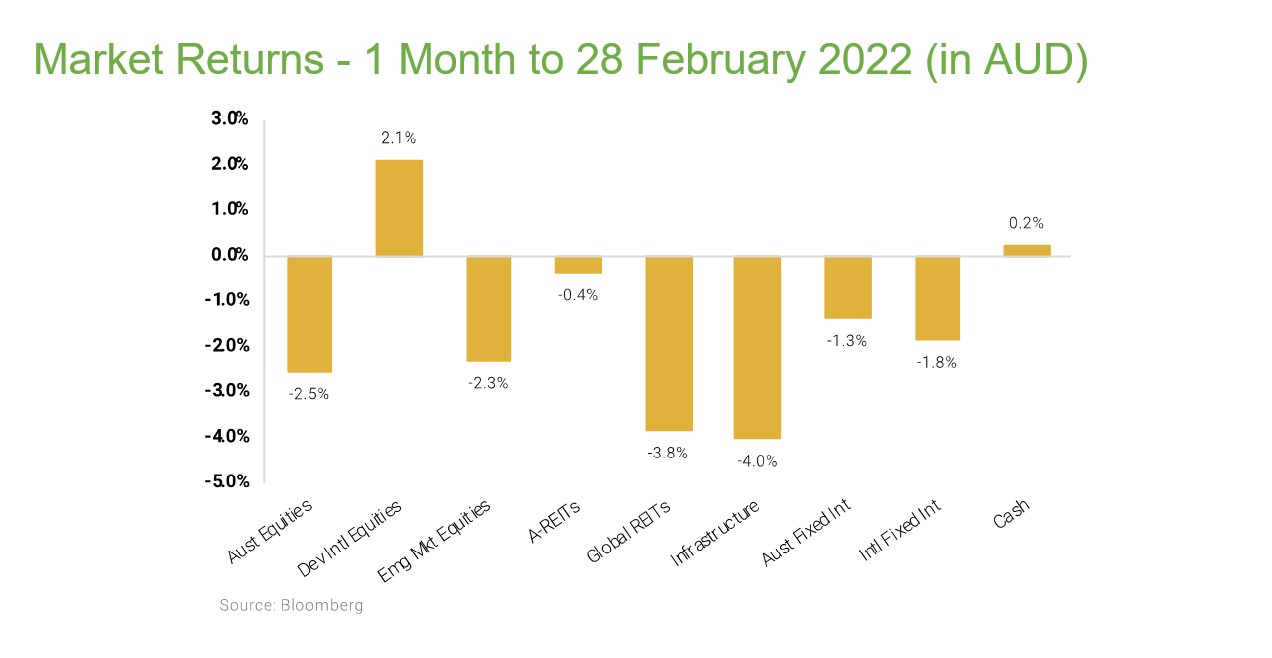

Markets have increasingly acknowledged residual inflationary pressures in the US, which became apparent throughout February. This leads to the follow-on thought that this will probably entail higher rates, which will in turn increase the probability of a harder landing. The February release for the US PCE inflation data tie a neat bow around this thesis with broad based inflation measures, covering core as well as volatile items like food and energy, printing higher than expected. Most categories of both goods and services were up strongly, and when you drill deeper the influences seem to be equally split between supply and demand pressures.

This has sent bond yields sharply higher, but markets have actually been better behaved in the last month than one might have expected in the face of stagflation (high inflation and lower growth) after the experience of 2022. This suggests some resilience, while of course a booming US economy and reopening China (albeit with a few speed bumps) will be helping as well. That said, these are also the markets that have been the most volatile and where traders have expressed their worries.

The final week of the month was extremely volatile with the S&P 500 bouncing within a 3% range. This was to a large extent driven by political and economic uncertainty in China and yo-yoing of the large Chinese tech stocks, despite a very strong earnings report from Alibaba. Taking a step back though, most equity markets haven’t given back that much of their gains from January, while Europe and the Nasdaq remain up 10% for the year.

For bond investors, who endured a particularly torrid 2022, January proved to be a false dawn, and most strategies gave up most of their January gains in February, with both government yields and credit spreads ending back where they were at the beginning of the year. We note though, that many local investors seem to have little duration (exposure to government bond risk) and have retreated to high quality floating rate corporate debt, which has been much steadier, and even hybrids have been relatively steady so far.

Looking Forward

We have been talking about scenarios for 2023 ad infinitum, which may sound like we are hedging our bets, because we are. The smartest people we know as well as the most important ones we don’t know (like Jerome Powell of the Federal Reserve) say that we are at a point in time where it is impossible to know what the near-term future holds as far as all important inflation (and hence rates) as well as economic growth are concerned.

It may also sound like we are indecisive and that is a little bit true, but we will have to come off the fence at some point and this is where the long-term nature of our asset class assumptions and their estimate of future risk premiums can be a help and a hindrance.

It is very clear, in our view, that there are certain asset classes like global small caps and emerging markets that are trading at market multiples, and they might reasonably be expected to trade at a premium given higher growth prospects.

Given 10 years they make a lot of sense but just before a potentially deeper than expected recession and in the middle of a steep rate hiking cycle where fragile economics of smaller companies or emerging market economies might be tested?