Steve Thaxter, Senior Partner and Principal Adviser

Sovereign Wealth Partners

Spoiler alert (and breathe a sigh of relief) – the research says yes, if we do it carefully enough!

Traditional portfolio theory tells us that there are optimum investment portfolio settings that give us the best long term return for the risk we’re prepared to take.

So when we start out, we establish a portfolio with careful allocations that give us the benefits of diversification along with the right risk and return mix. But over time, the dynamic nature of markets always pushes our allocations off track. Some sectors do better than others.

So we need some sort of rebalancing process to continue to assess the opportunity going forward whilst staying within the risk expectations initially agreed.

Therefore in our review meetings we tend to adjust our clients’ current portfolio exposures towards asset allocation targets. More often than not we do this annually. But have you ever wondered if you were missing out by not rebalancing your portfolio more frequently? Or should you jump in and rebalance straight after a big market move?

New research by Vanguard in the US looks at the frequency of rebalances and the impact on return. The research looked at:

- time based rebalancing – daily monthly, quarterly, annually, biannually and never;

- threshold based rebalancing – rebalancing when market moves meant that allocations were “out” by more than 1%, 3%, 5%, and 7%

- combination rebalancing – combining the two

The results were surprising. The costs of micromanaging with frequent rebalancings far outweighed the benefits.

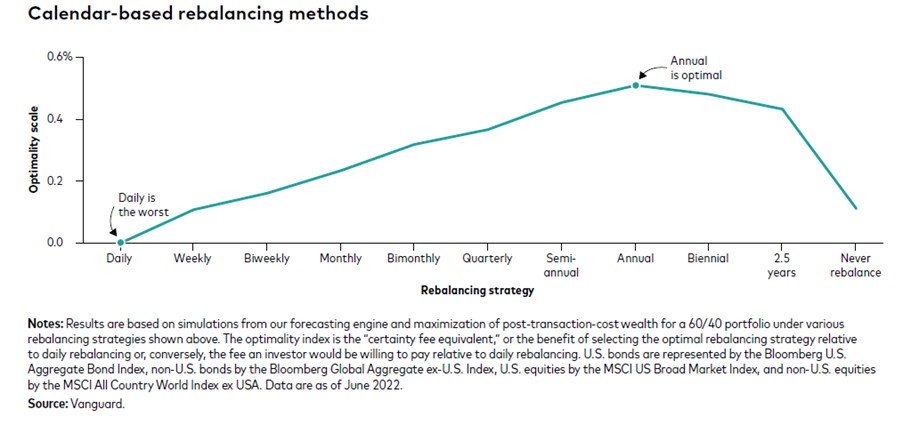

When looking at time-based rebalancing alone, annual rebalancing came out the best:

And again, with combination rebalancing, irrespective of the movement threshold, annual rebalancing was better than monthly or daily. Best of all was annual rebalancing to a low threshold.

We find it interesting that rebalancing straight away after a big market move is not necessarily optimal. The study found that rebalances during volatile markets were expensive and quite likely to be reversed at the next rebalancing, which adds to costs.

It’s not the full story of course, there’s much to be said for taking opportunities in fearful markets and strategies such as tax loss harvesting. But for us, this research re-enforces why we take such a careful approach to asset allocation at our annual review meetings.