Sovereign Wealth Partners and InvestSense Pty Ltd

Market Commentary

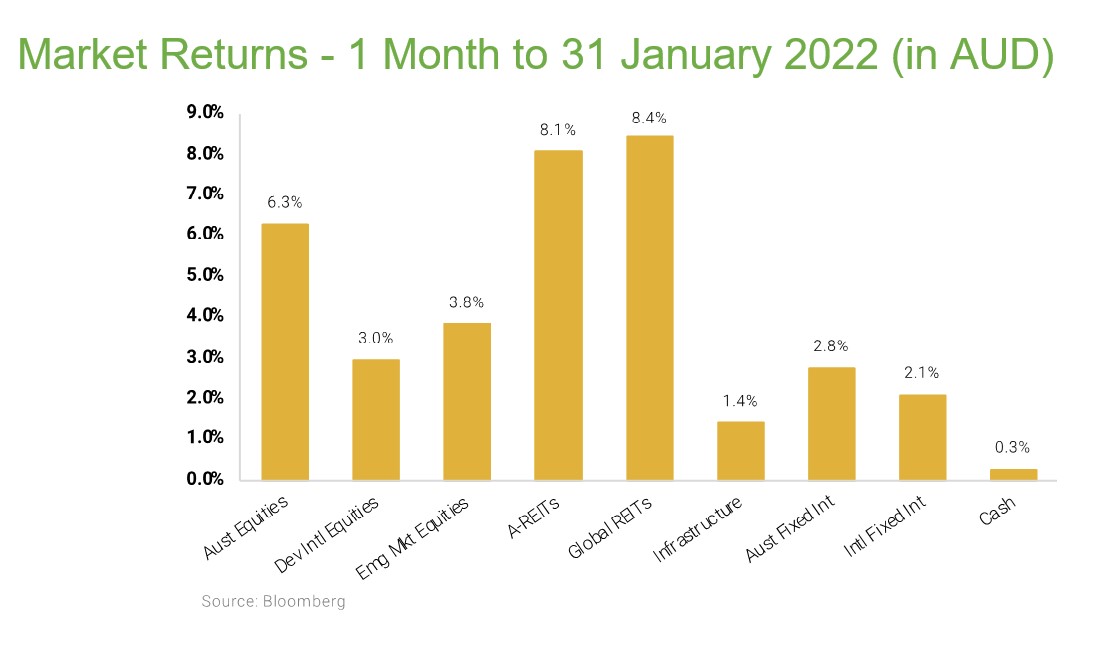

Buoyant markets returned throughout January with most major equity markets up 5-10% for the month. So far this year, the dominant (and very positive) have been all about moderation, specifically that of inflation and economic growth. The inflation part is obvious, as receding inflation pressures from supply side factors such as energy and traded goods are universally a positive thing, and something which investors hope will lead to lower rates – which is particularly important given how much debt there is around. The hopes of the market vis-a-vis economic growth are more nuanced, as too much growth would again put upwards pressure on wages, services inflation and ultimately interest rates. A hard recession, like going to the dentist, is not something anyone is going to look forward to, even if it is deemed necessary. So, the prospect of a soft recession is the new goldilocks and the thing that markets are now pinning their hopes on.

Generally, the US earnings season has, as expected, got off to a lacklustre start. However, many companies have still managed to inch above dismal expectations, while investors remain on tenterhooks about the prospects for later in 2023. Forward guidance therefore becomes the swing factor, and this is why the market reacted so negatively to Microsoft’s okay results and dour outlook. Happily, though, the macro-backdrop has been subtly improving, and there were a few 4th quarter data points that came out last week which pointed to better-than-expected economic resilience. GDP figures published last Thursday suggested the US economy is slowing, but not precipitously so. While labour markets remain tight, the latest inflation gauge (the US Fed’s preferred Personal Consumption Expenditures report) released on Friday was as benign as could be expected. Traded goods inflation continues to decline, while services inflation was flat across most categories. There is also increasing optimism that China will forge ahead with its ambitious reopening strategy, which conveniently means the Chinese economy might well be in a position to pick up the slack if and when the US economy slows more appreciably later in 2023. This is about as good an outcome as the Fed and investors could hope for right now and increases the chance of a soft landing.

Meanwhile in Australia, the inflation numbers for the last quarter, also published last week, were higher than most expected, even if slightly lower than the RBA had forecast. The trimmed mean measure (which removes the most volatile items) was up by 1.7% (7% on an annualised basis) and just a touch down from the previous quarter. Bond yields jumped around 0.3-0.4% across the yield curve, but that got them back to just where they had been only a few weeks ago. During the past two years the Australian economy has tracked behind the US by about 6 months and if that script continues then the RBA might succeed in having the Fed do the hard lifting without having to break the local housing market. So far inflation does not appear to be waning in the way that it has in the US, and a resurgent Chinese economy could yet put a spanner in the works. Either way it will be a close-run thing, but the RBA remains optimistic and just today confirmed that they believe that last week’s 4th quarter inflation print marked peak inflation. It’s a brave call but if they pull it off, they will have won back a lot of credibility, and for now the market believes them.

Medium and long-term interest rates were down by almost 0.5% here and overseas throughout the month, which pretty much explains why the Nasdaq was up 10% in January despite slowing revenues amongst the large tech stocks. European and Asian indices were also up by a similar amount, also helped by Chinese reopening, while Japan, Australia and the UK were all up by around 5% for the month. Commodities markets (ex-energy) have also been strong this year, not least iron ore, and the three largest local miners accounted for almost half of the ASX’s gain, with the large banks also posting strong high single digit returns, which actually left the rest of the universe looking a little lacklustre. There were some notable exceptions in the consumer staples and discretionary sectors including James Hardie, Woolworths, Wesfarmers and Aristocrat Leisure. Real estate trusts also enjoyed the less dour economic outlook and prosect of less interest rate rises, with industrials like Goodman Group up by almost 15%, while the office and retail sectors were a little more subdued.

Lastly, it was also a much better month for bond investors, with government bond portfolios clawing back 2-3% and corporate bond investors also benefitting from tighter credit spreads that reflect the likelihood of a less severe 2023 recession.

Looking Forward

Around the traps we hear more and more about a potential regime change, and if inflation and interest rates are the ‘prima causa’ of investment regimes then this seems plausible. For this reason, we have been doing a lot of work on scenario analysis internally and in collaboration with the economists and managers we work with, on the basis that this might be a particularly good year to think broadly and flexibly, not just about what happens in 2023 but over the longer term.

Another, perhaps more subjective, theme that we are picking up on is a perennial favourite – the imminent ‘stock pickers market’. Except this time, we think it might have legs, especially if we are amid a regime change. At such times, the index portfolio inevitably ends up being heavily weighted towards things which are suddenly less prospective and quite expensive (think Nifty Fifty stocks of the sixties, Dot Com stocks or real estate stocks and banks in 2007). This would give (some) active fund managers a bit of tailwind but, there are also some more tangible pointers to where some styles and regions could have an easier ride because of valuation starting points rather than just relying on a change of tide that benefits active management generally.