Sovereign Wealth Partners and InvestSense Pty Ltd

Market Commentary

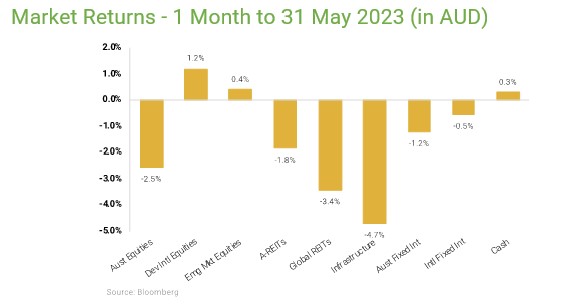

In markets, May 2023 was the month that the AI theme really broke cover in markets. Nvidia’s blow-out result at the end of the month seemed to cement the notion that this theme represents more than just hope for the future – people are using the technology and others are making vast sums of money. However, it still remains early days and opportunistic capital has gravitated to an arrow subset of large US tech titans and smaller, mainly US-domiciled, software/hardware stocks that are seen to have a network and first-mover advantage respectively. As a result, overall market gains excluding these stocks were actually fairly muted for the month, and indeed for the year to date, while the technology-based Nasdaq was up 10% (and some 30% for the year). Most other markets, with one exception, were actually in negative territory in May. The exception was Japan, which has been quietly growing earnings momentum for the last few years but really took off in early May as Warren Buffet’s interest seemed to spark investor enthusiasm. As the debt ceiling negotiations progressed and a resolution seemed imminent a much broader rally in markets gathered pace in the last few days of last week, after the month end.

The worst-performing market was the UK where the FTSE 100 was down more than 5%. While the headlines about inflation and the onset of a wage-price spiral won’t have helped sentiment it was really the negative performance of the large global energy, banking and consumer staples stocks in this index that drove the lacklustre returns. While Australia was down over 2% last month this was pretty much in line with most other markets (including the US ex-IT stocks), which all traded more or less in line without moving very much either way. However, the trends were similar to the UK with the large banks and materials stocks weighing on returns as, outside of some large US tech stocks, the world weighs up the impact of a likely recession later this year or in 2024 (most surveys and quantitative frameworks put the probability of recession in the next 12 months at around 75%). As these expectations firmed, energy prices and most other commodities were also on the back foot during the month with modest declines across the board.

The other main talking point in markets is the fact that bond yields have started to drift up again. The US market sets the tone and there is growing recognition that there are pockets of stubborn, mainly services-based, inflation that may force central banks to maintain current levels of interest rates and even lead to more rises. Even the debt ceiling deadline has passed without too much bond or equity market drama but it has forced the US government to run down its cash account (the Treasury General Account). The US Government will now have to issue more debt to rebuild these reserves and that is also putting upwards pressure on yields. Over the past month or so this has led to increases in short-term rate expectations in the US with one or two more 0.25% rises expected in the US by year-end. In Australia, similar conditions have led to an expectation of one more 0.25% hike as opposed to hopes for a reduction of rates by 0.25% in 2023 just a few weeks ago. This means rates are now expected to peak in the US and Australia at about 5.25% and 4.25% respectively by year-end. After that time, they are expected to decline suddenly as that recession kicks in. Anything on either side of this prognosis could surprise quite a lot but for now corporate bond spreads (often the canary in the recessionary coal mine) have remained sanguine, even tightening slightly in May.

Looking Forward

As we mentioned in the May market update there is a lot to interpret in manager performance and, put simply, manager research ‘got real granular’. However, this AI theme and the alacrity with which markets have reacted has forced us to bring forward some of the thematic research we have had on the back-burner – what does the world look like once the effects of COVID policies have worked their way through the system. The intersection between these thoughts is that it is a very good time to be talking to quite a few managers that are focused on growth about what the ‘manufacturing’ side of this AI boom looks like. That means talking to managers about individual software and hardware beneficiaries and trying to work out how much of this is priced in already and what has to happen for current valuations to make sense.

There was a lot going on last year but at least you knew where you were with respect to different investment styles – growth managers were interest-rate sensitive (and very much on the back foot in a rising interest-rate environment) while value managers were enjoying a renaissance with robust valuations proving defensive. This year falling energy prices and troubled US banks have affected value managers in very different ways while growth managers’ relative performance has been entirely driven by how exposed to AI they are (many that had pulled their horns in have struggled to keep up with the rebound). All of this points to the need for more granular and intensive research and to the need to understand exactly what a manager is exposed to rather than relying on a view of what outcomes you think their process should lead to.

DISCLAIMER

This document or content within or attached has been prepared by InvestSense Pty Ltd ABN 31 601 876 528 Authorised Representative of IS FSL Pty Limited AFSL 408 800. The information contained in this report is obtained from various sources deemed to be reliable. No representation or warranty is made concerning the accuracy of any data or calculations contained in this document and should not be relied upon as such. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this document. Past performance information given in this document is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance. This document must not be disclosed or made available to any person without the permission of InvestSense Pty Ltd. This documents provides general information only and has been prepared without taking account the objectives, financial situation or needs of individuals. Before making an investment decision, investors should consider the appropriateness of this information, having regard to their own objectives, financial situation or needs or consult a professional adviser. This document or content within or attached is for Financial Adviser use only. © 2022. This publication is subject to copyright of InvestSense Pty Ltd. Except for the temporary copy held in a computer’s cache and a single permanent copy for your personal reference or other than in accordance with the provisions of the Copyright Act, no part of this publication may, in any form or by any means (electronic, mechanical, micro-copying, photocopying, recording or otherwise), be reproduced, stored or transmitted without the prior written permission of InvestSense Pty Ltd.