Sovereign Wealth Partners and InvestSense Pty Ltd

Market Commentary

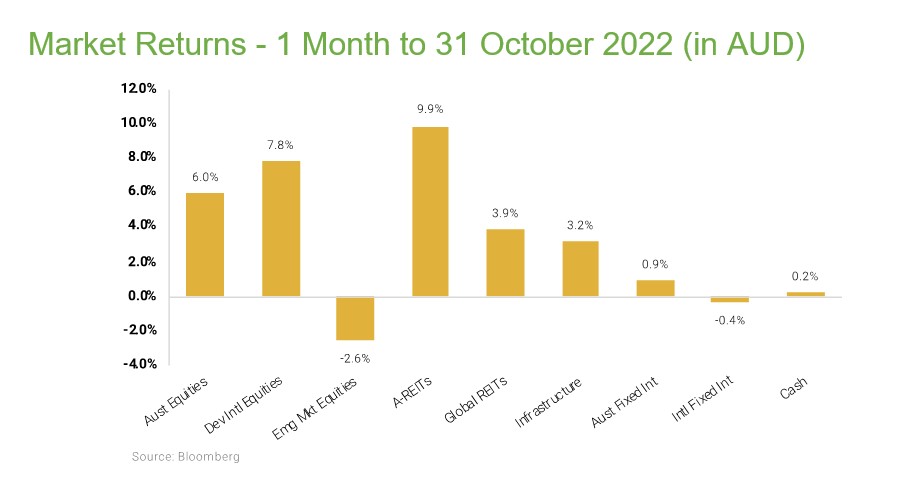

Markets capped a very strong month for an apparent kaleidoscope of reasons including not as dismal as expected earnings, anecdotal evidence of slowing inflationary pressures in the US and even some economic resilience in recession bound and energy starved Europe.

Against these ‘almost positives’ there was enough in the news to make a near 10% rise in markets during October seem improbable on the face of it – including an overall increase in inflation (and medium-term interest rate expectations), tightening US dollar liquidity conditions, a deepening of economic woes in China (not to mention the geopolitical implications of a harder line Chinese Communist party after the recent 5-year congress) and an ever more belligerent Russian leadership.

However, investor and consumer sentiment had, by the end of September, reached the lows of the GFC, post Dot Com recession as well as the depths of the COVID (market) crisis. From there it doesn’t take much to lighten the mood, and ironically it was probably the idea that difficult times ahead might slow the pace of interest rate rises that had the most impact – along with some lingering inflation – that have put a fire under markets. So even though rates appeared to head higher during the month, inflation expectations rose by more, so real (after inflation) rate expectations started to come down.

Towards the end of the month, it was the turn of some of the former market darlings to come under pressure, even though they have traditionally benefited from lower interest rates. Meta (Facebook), Google and Amazon all fell dramatically when they reported sharply lower earnings while Apple was rewarded for keeping tech hopes alive. At the other end of the spectrum the biggest gainers were amongst real estate trusts, consumer staples and banks.

Similarly in Australia, bombed out local real estate trusts also enjoyed a boost from the notion that we might get the inflation without all of the interest rate pain, but the biggest contributors during the month were the banks. ANZ’s earnings result confirmed the improvement in net interest margins currently being enjoyed by the Big Four, as mortgage rate rises have outpaced increases in rates paid to depositors (perhaps not something they are wanting to shout from the rooftops). Both sectors ended up around 10% for the month, along with energy stocks which continued to benefit from the supply squeeze in Europe. With iron ore prices suffering from a weaker Chinese outlook, materials were the main drag on the index, leaving the local market up by a relatively modest 6%.

The Japanese market produced a similar return while the UK market lagged slightly, but all of these markets got there without too much volatility along the way. Europe and the US on the other hand have proved to be the lightning rod for investor sentiment and ended the month up 9% and 8% respectively in local currency terms, while the US market was especially volatile. The Euro also fared relatively well, adding to the sense that investors are seeing value in a region where sentiment has probably been the worst.

The other surprise during the month was the strength of local bond market, where yields started to drift down even as they edged higher around the rest of the world. Most striking was the fact that during this period the RBA surprised the market with a smaller than expected 0.25% rate rise, while September’s inflation print came out ahead of expectations, exhibiting much of the services-based pressures that the US has been faced with in the last 6 months. Also, somewhat counterintuitively, credit spreads eased during the month even as global recession fears mounted, and many investors will be hoping that both the bond markets and equity markets are sniffing out a less pressing rate rise schedule along with a softer landing.

Looking Forward

One facet of the current market that we are thinking about is not only bond markets and the real rate of interest but the increasing policy and rate divergence between here and the US.

In recent years (and in fact most of the time) the Australian bond market is a slave to that of the US but in recent months we have seen some quite significant divergence and we are rapidly heading back to negative rate territory, aided and abetted by a suddenly dovish local central bank.

This was somewhat surprising, and we got another piece of the jigsaw when the RBA announced its rate decision shortly after month end. In the meantime, we will be talking to savvy bond managers, and more specifically we will be updating our ‘peeling the mortgage rate onion’ piece from earlier in the year.

We could say that half of that analysis proved prescient (rising global rates and somewhat rising local funding costs), but the relative plateauing of local medium term borrowing costs has been surprising. Local mortgagees probably don’t feel as if they have got off lightly, but in many respects that is the case, and it will be interesting to update the analysis with this new information.