Chris Forrest – Senior Partner

Sovereign Wealth Partners

Recently we listened to Chris Watling of Longview Economics.

The thing which caught our attention was good old-fashioned monetary theory. It seems that the vast majority of the market drank the cool-aid view that high inflation was solely caused by COVID induced supply disruption and was therefore transitory.

This wasn’t entirely untrue, until it was. As reserve banks maintained ultra-low interest rates whilst governments pumped record levels of support money into their economies (which were brought to a near standstill by the pandemic), the tinder box was built waiting for the spark to come along. That spark was Russia declaring war on Ukraine.

But some monetarists were onto the risk in advance of this:

“I have argued that an annual rate of US consumer inflation of between 5% and 10% is to be expected until the end of 2022. The reason is that the American economy has a monetary overhang from the almost 35% growth of the quantity of money in the two years to mid-2021. Even if inflation does eventually (in 2024 or 2025?) drop back to 2%, that surely stretches the notion of “transitoriness” to silliness…. In qualification, upward pressure on inflation is less pronounced in the Eurozone and the UK than in the USA, and wealth still in Japan than in Europe.”.

Source: Institute of International Monetary Research, https://mv-pt.org/monthly-monetary-update/ September 2021

Reserve banks are now onto this.

So what now?

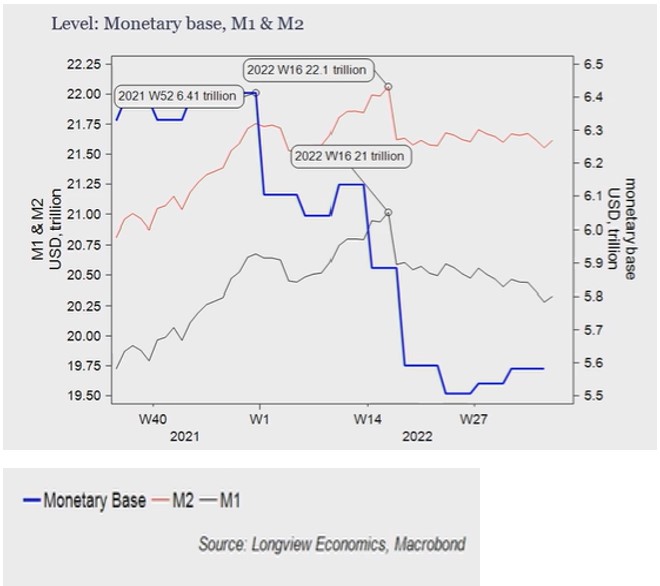

Money supply peaked in the US around March this year and has been contracting since. The important lines in this chart are M1 and M2.

What does this mean? Quite simply, money on issue is shrinking. What we know is that monetary policy works with long and variable lags and so the actions today will be reflected in time. The contention is that between shrinking money supply and raising rates, the US Federal Reserve will overachieve and drive the US into recession – the only question is how deep. (Market volatility suggests this unknown is keeping traders awake at night).

How does it work?

The transmission mechanism goes something like this: monetary conditions tighten then financial conditions tighten then credit (lending) conditions tighten and, if conditions are tight enough, recession occurs. This may take up to a year to hit in the United States and, hitting the largest economy means it will impact the world economy. We’ve all heard the expression “If America sneezes, the world catches a cold.”

So will reserve banks overcorrect? Will they compound their errors? Perhaps. The governor of the federal reserve said just a month ago “Money supply data doesn’t have a big message for monetary policy” – or does it? If indeed he is wrong, the US may have more than a shallow recession. Based on his hawkish tone, the trajectory isn’t changing anytime soon.

What about Australia?

The Reserve Bank of Australia’s preferred published measures are M3 and broad money, other measures of the monetary base. They also publish it in terms of growth rather than absolute levels. For the purpose of this article, it illustrates the same point.

It’s clear the money base expanded significantly in 2020/21 in response to the pandemic as did credit on a lagged basis. At the very end of the chart, money supply growth is just rolling over. If the RBA keeps tightening conditions, we can expect to see credit roll over as well.

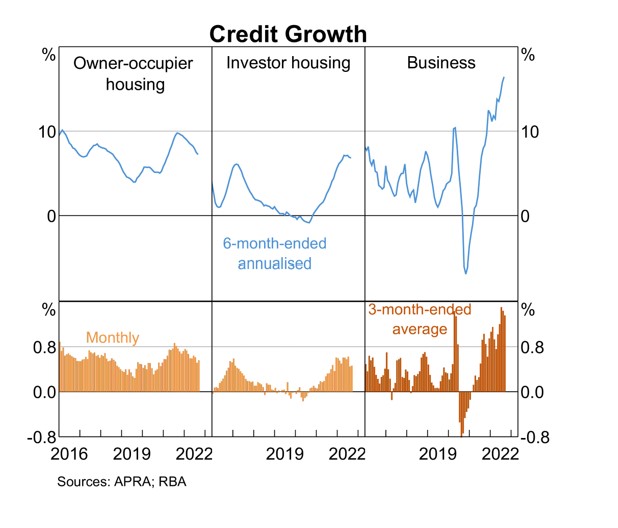

To the point of credit conditions tightening, the following chart shows housing credit growth has already started to slow but business is yet to react. The consumer is the first responder and we expect business to follow in short order.

Conclusion

Australia is lagging the US and our Reserve Bank may not have to do as much to have the desired impact. Whilst the RBA didn’t utilise quantitative easing anywhere near the scale of the US, a decline in the growth of money supply is likely to stymie the economy and have an impact on inflation in tandem with tighter interest rate policy and fiscal policy.

Another key point worth remembering is a key difference in the transmission mechanism of interest rates. US mortgages price off the 30 year rate which means interest rates may have to go higher before they have an impact. By contrast, Australian mortgages are priced off the cash rate and so rate rises are felt almost immediately.

The bottom line is this: reserve banks probably won’t navigate this as well as we would like and may overtighten monetary conditions. This will impact the economy and jobs and so investors should be judicious and patient waiting for opportunities to present themselves.

Definitions:

M1 = money supply including cash, currency demand deposits and other liquid deposits.

M2 = M1 plus “near money” which can be savings deposits, money market securities and other deposits. These assets are less liquid than M1. (Quantitative activity would be captured in M2).